Despite inroads working women have made in recent years, according to the American Association of University Women (AAUW), on average, they still earn 16% less than men — 84 cents for every $1 a male counterpart earns. The gap is wider for working mothers. A report from the National Women’s Law Center found year-round, full-time working mothers are typically paid 71 cents for every dollar paid to year-round working fathers. What’s at work here? For many young women, it can be these financial misconceptions.

I’M TOO YOUNG TO SAVE FOR RETIREMENT

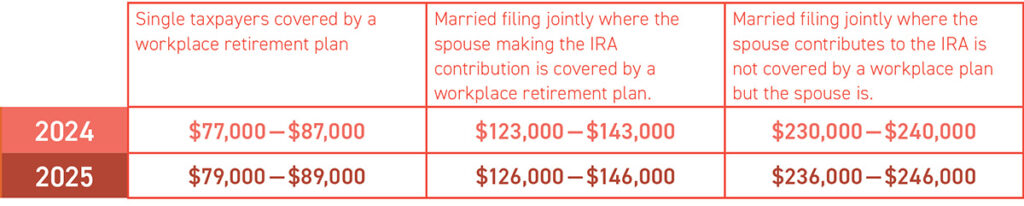

Retirement savings may be a low priority at the beginning of a career. But it’s never too early to take advantage of the power of time and compound interest. Open an Individual Retirement Account or join your employer-sponsored retirement savings plan. If your employer matches contributions, contribute at least the match amount to maximize your savings.

I DON’T HAVE ENOUGH MONEY TO INVEST

No amount is too small to start a regular investment program. Creating a relationship with a financial professional now can help you find suitable investments based on your financial situation and give you a foothold in future success. Take this opportunity to financially plot a plan for life events such as unexpected emergencies, buying a home, or starting a family.

DEBT IS BAD

Paying credit card bills in full when due avoids interest and allows you to build credit. A good credit score can lead to better interest rates on mortgages, car loans, etc.

Personal finance can be complex and present unique challenges, especially for women.

Talking with a financial professional can help you navigate these challenges.