The higher your income, the more complicated the options. Generally, deductible IRA and Roth IRA contributions aren’t permitted if you have a 401(k)/403b/457 retirement savings plan at work.

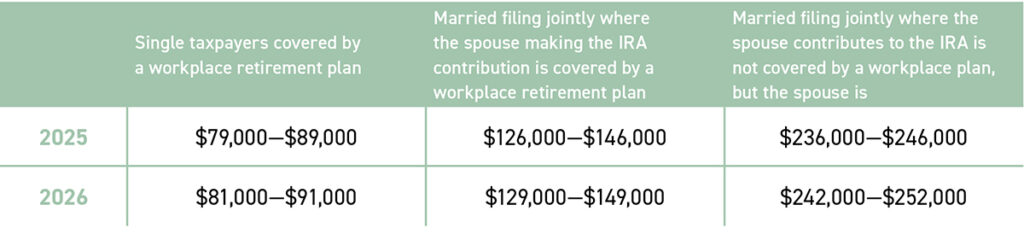

In 2025, individuals with a modified adjusted gross income (MAGI) of $89,000 or more ($91,000 in 2026), and married couples filing jointly with a MAGI of $146,000 or more ($149,000 in 2026), cannot make deductible contributions to a traditional IRA. Roth IRA contributions ignore workplace retirement plans, but singles and those married filing jointly become ineligible with MAGI of $165,000 and $246,000 or more ($168,000 and $252,000 in 2026), respectively. However, if your employer’s plan allows you to choose between a traditional or Roth employee retirement savings plan, these contributions aren’t subject to any income limitations. So, how do you decide? Here are some factors to consider with your trusted professional.

- Your current and future tax situation

- Nonretirement investments

- A Roth conversion if you’re nearing retirement

- Splitting retirement plan contributions between traditional and Roth accounts

- Starting this year, high-income retirement plan savers over 50 years old must make any employee deferral catch-up contribution as a Roth contribution