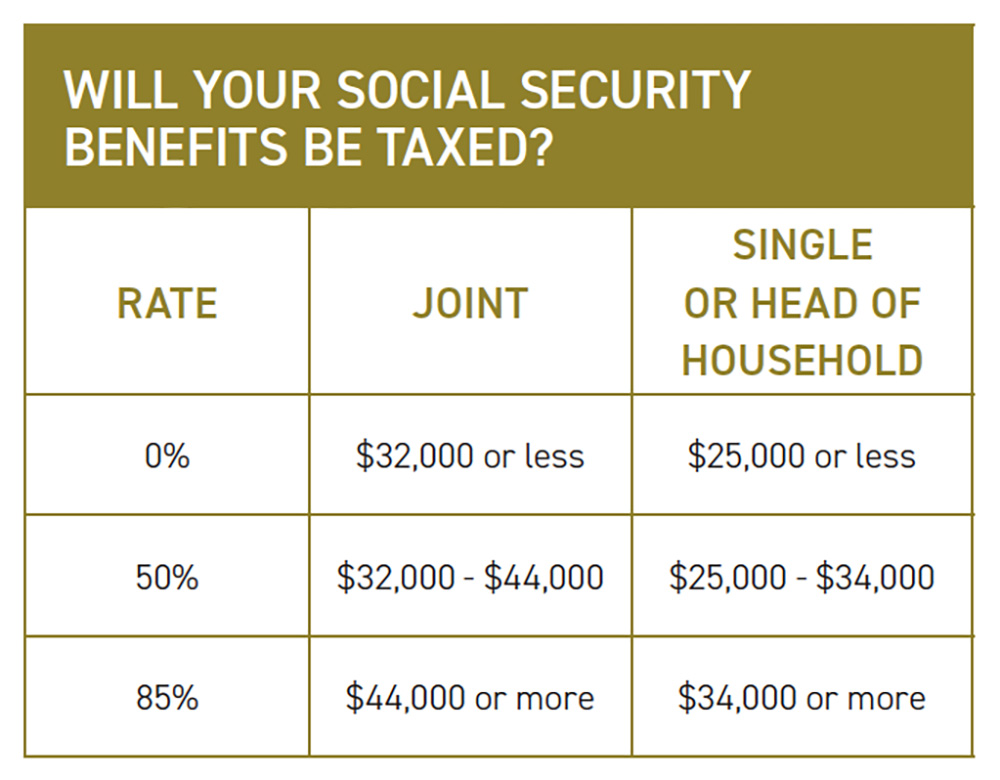

Minimize taxes. Maximize returns. Knowing how to manage taxes can significantly enhance your overall financial strategy, helping you retain more of your hard-earned income.

TAX-ADVANTAGED ACCOUNTS

If you aren’t already doing so, one of the simplest ways to trim current taxes is to maximize contributions to an employer’s retirement savings plan, individual retirement accounts (IRAs), or health savings accounts (HSAs). You can deduct contributions to these accounts from your taxable income, and the growth is taxdeferred or tax-free, depending on the account type.

Let’s say you invested tax savings of $1000 a year in stocks as represented by the S&P 500 over the past ten years ($10,000 total). You could have more than doubled the invested tax savings to $20,160.

TAX-LOSS HARVESTING

If you have realized gains in your portfolio, consider strategically realizing losses to reduce your overall tax. However, be aware of the wash sale rules. These rules prevent you from taking a loss on a security if you buy a substantially identical security within 30 days before or after the sale. You can avoid triggering the wash sale rules while maintaining the same portfolio allocations by selling the security and waiting at least 31 days before repurchasing it or selling the security and buying shares in a mutual fund that holds similar securities.

HOLDING INVESTMENTS LONG-TERM

Gains on assets held for less than a year are taxed at your ordinary income tax rate, which may be as high as 37%. For long-term investments, those held for more than one year, you generally pay capital gains tax at 0%, 15%, or 20% depending on your other taxable income.

INVESTING IN MUNICIPAL BONDS

Municipal bonds,* or “munis,” can be an attractive option for reducing tax liabilities. The interest earned on most municipal bonds is exempt from federal income tax and, in some cases, state and local taxes as well. This makes them a strategic choice, especially for investors in higher tax brackets.

Before using any tax-trimming strategies, talk with your trusted advisor. They can help you identify deductions, credits, and other techniques that suit your specific financial situation and investment goals.

*Prices of fixed-income securities may fluctuate due to interest rate changes. Investors may lose money if they sell bonds before maturity. Before investing, read the prospectus and consider the fund’s investment objectives, charges, expenses, and risks.