One simple step can lower your tax bill and boost your retirement savings. The actions you take today to prepare for retirement will influence your financial situation in later years. Contributing to an eligible retirement account by the April 15, 2026, income tax deadline will reduce your 2025 taxable income by the amount you contribute.

INDIVIDUAL RETIREMENT ACCOUNT

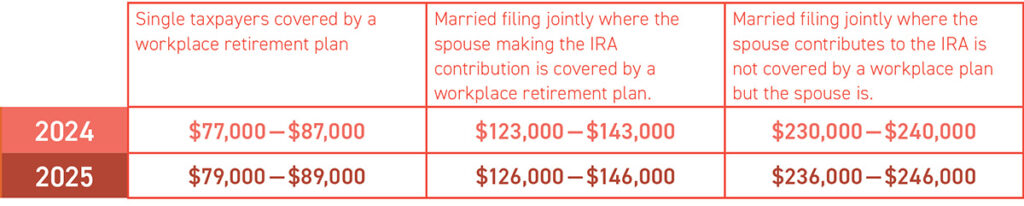

An Individual Retirement Account (IRA) gives you the flexibility to choose from various investments to hold in your account. For 2025, you can contribute up to $7,000 — or $8,000 if you’re 50 or older. In 2026, the contribution limit increases to $7,500 — or $8,600 if you’re 50 or older. You must have “earned income,” including money from wages, salaries, tips, bonuses, commissions, or self-employment income, to contribute to an IRA. Your spouse can also contribute to an IRA.

SIMPLE IRA

A Savings Incentive Match Plan for Employees, or SIMPLE IRA, is a retirement savings plan designed for small businesses with 100 or fewer employees. Employers must match employee contributions dollar-for-dollar — up to 3% of an employee’s compensation — or make a fixed 2% contribution for all eligible employees, even if an employee chooses not to contribute. Employers may also make additional nonelective contributions beyond the standard 2% nonelective or 3% matching contributions.

If you’re aged between 60 and 63, you can make a catch-up contribution of up to $5,250 in 2025 and 2026.

As with a traditional IRA, you can contribute to a SIMPLE IRA until April 15th following the end of the tax year and benefit from the tax deduction.

SOLO 401(K)

Solo 401(k) plans are designed for a business owner with no employees and their spouse. You can make elective deferrals of up to 100% of your earned income or the annual contribution limit, plus employer nonelective contributions of up to 25% of compensation.

Contributions can be made until the company’s tax return deadline, including extensions. Financial and tax professionals can help you determine which plan is right for you.